Google Stock: The Undervalued Tech Giant Poised to Dominate the AI Revolution!

Discover why Alphabet's innovation in AI, robust financials, and market dominance make it a once-in-a-decade investment opportunity despite looming regulatory challenges.

Alphabet Inc. (GOOGL) has demonstrated robust financial health and operational growth. Key financial highlights include:

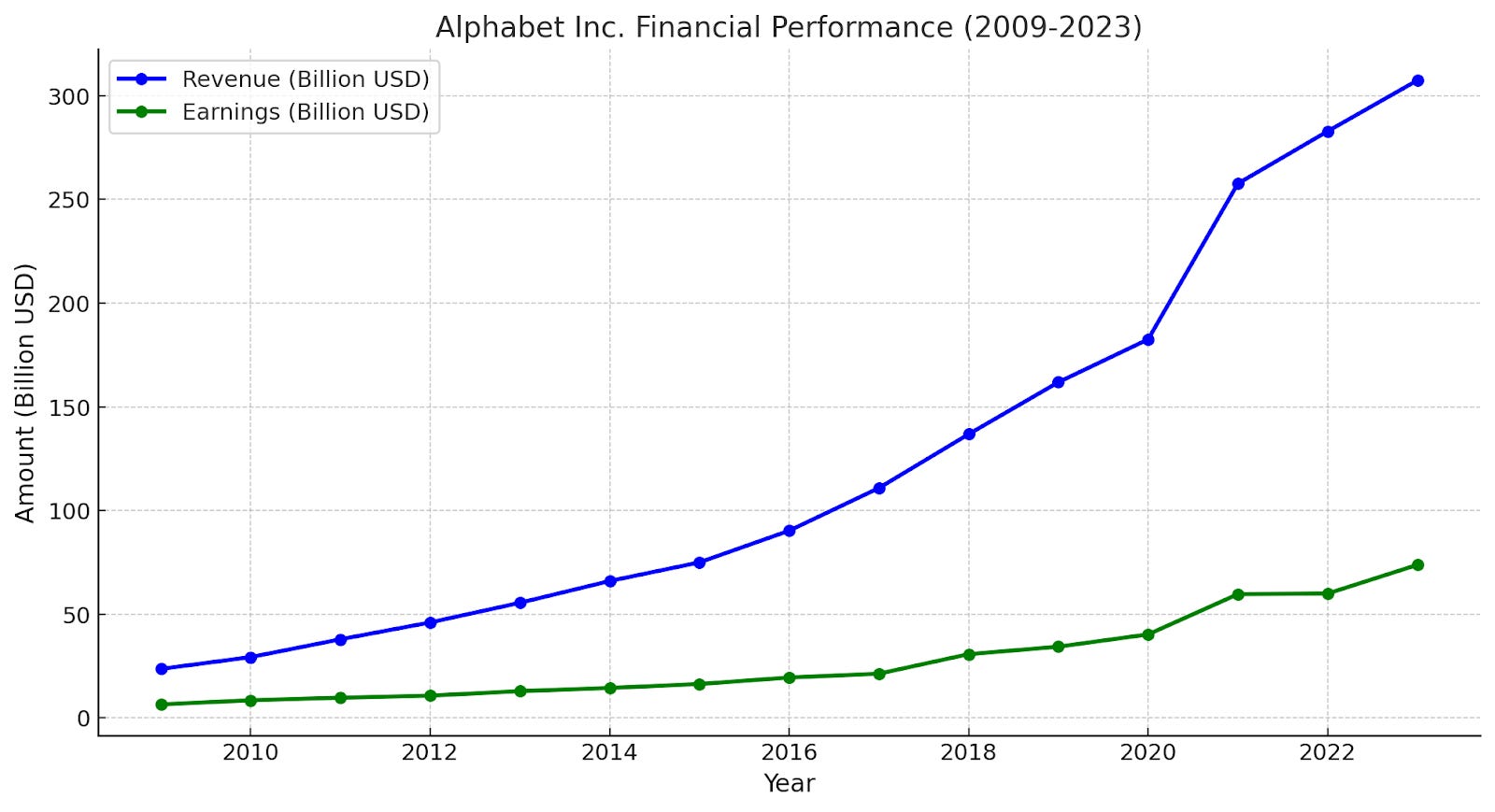

2023 Revenue: $307.39 billion, marking an 8.68% increase from the previous year.

Earnings: $73.80 billion, reflecting a 23.05% growth year-over-year, bolstered by strong performance in core businesses like advertising and cloud computing

The stock is currently trading around $140 per share, and analysts forecast a 12-month price target of $205-$206, indicating a potential upside of approximately 17%-18%.

Is Alphabet Undervalued?

Based on financial metrics, Alphabet appears to be undervalued.

The company's price-to-earnings (P/E) ratio and its growth in critical areas like AI and cloud services suggest strong intrinsic value.

Analysts and market strategists describe Alphabet as a "growth stock trading like a value stock", making it an attractive long-term investment for those comfortable with potential regulatory risks

Recommendations

For Long-Term Investors: Given Alphabet’s strong fundamentals and growth prospects, current prices represent a potential buying opportunity.

For Risk-Averse Investors: Consider regulatory risks and diversify portfolios to mitigate potential impacts.

Key Charts to examine Future Growth Potential

Alphabet Inc.'s Financial Performance (2009-2023):

This line chart shows the steady growth in both revenue and earnings over the past 15 years, highlighting Alphabet's strong financial trajectory.

Alphabet Inc.'s P/E Ratio Changes (2009-2023):

This chart tracks changes in Alphabet's price-to-earnings ratio, providing insight into valuation trends over time.

Why this is important: The high P/E ratio here seems to indicate that investors expect significant growth. Also a growth over time shows that optimism for Google stock remains strong

Tracking P/E over several years allows us to:

See how the stock performs during different economic cycles.

Understand how external factors (e.g., recessions, bull markets, industry disruptions) influence valuation.

Google is performing well against its competitors

Alphabet (Google) has maintained a dominant position in the search engine and digital advertising markets over the last 15 years. Its primary competitors in various sectors include:

Microsoft (Bing): Competes in search engines and cloud computing.

Amazon: Challenges in cloud computing and digital advertising.

Apple: Competes in mobile ecosystems and hardware.

Meta (formerly Facebook): Rivals in digital advertising and social media.

Baidu: Dominates search in the Chinese market

Market Share (Search Engines): Google consistently holds over 90% of the global search engine market, while competitors like Bing and Yahoo have single-digit shares. Baidu leads in China, and Yandex in Russia.

2023 Market Snapshot: In 2023, Google Search commanded 81.95% of the desktop search market globally, followed by Bing (10.51%) and Yahoo (1.36%). On mobile, Google's share was even higher, reflecting its strong integration with Android devices.

Key Conclusions from a SWOT Analysis

🟢Strong Fundamentals Drive Long-Term Growth

Alphabet's diversified revenue streams, financial stability, and leadership in digital advertising, AI, and cloud computing position the company for sustained growth. Its consistent earnings and revenue growth underscore its resilience and operational efficiency.🟢 AI Leadership and Innovation as a Catalyst

Alphabet's significant investments in AI (e.g., Google Bard, TensorFlow) and partnerships in cloud services reflect its ability to capitalize on emerging technologies. This innovation should provide new revenue streams and strengthen its competitive moat.

🟡Regulatory Challenges Remain a Key Risk

Ongoing antitrust and privacy-related regulatory scrutiny could lead to fines, operational changes, or increased compliance costs. These risks may pressure margins and investor sentiment.

🟡Advertising Dependency and Economic Sensitivity

While Alphabet's dominance in digital advertising is a strength, its reliance on this sector makes it vulnerable to macroeconomic downturns, changes in consumer behavior, and evolving privacy regulations.

🟢 Valuation Suggests Upside Potential

Alphabet's current valuation metrics, including its price-to-earnings (P/E) ratio, suggest that the stock may be undervalued relative to its growth prospects. The projected upside of 17%-18% aligns with analyst expectations for continued stock price appreciation.

Recommendations for Investors

Long-Term Investors: Consider Alphabet as a core portfolio holding, leveraging its consistent growth and undervaluation. Stock is undervalued in our opinion!

Risk-Averse Investors: Diversify to offset potential regulatory or macroeconomic risks.

Growth-Oriented Investors: Look to capitalize on Alphabet’s innovations in AI and cloud computing for future gains.

By balancing its strengths with awareness of potential risks, investors can make informed decisions about Alphabet's stock as a growth-oriented opportunity.

Disclaimer: This article is for educational and entertainment purposes only. It should not be considered financial advice, and readers should consult with a qualified financial professional before making any investment decisions. The opinions and information presented here are based on publicly available data and are not intended to serve as an endorsement or recommendation of any particular investment. Always do your own research before investing